Roof Depreciation Life Rental Property

Depreciation Recapture On Rental Property And Calculator Avoid The Painful Irs With A 1031 Exchange Inside The 1031 Exchange

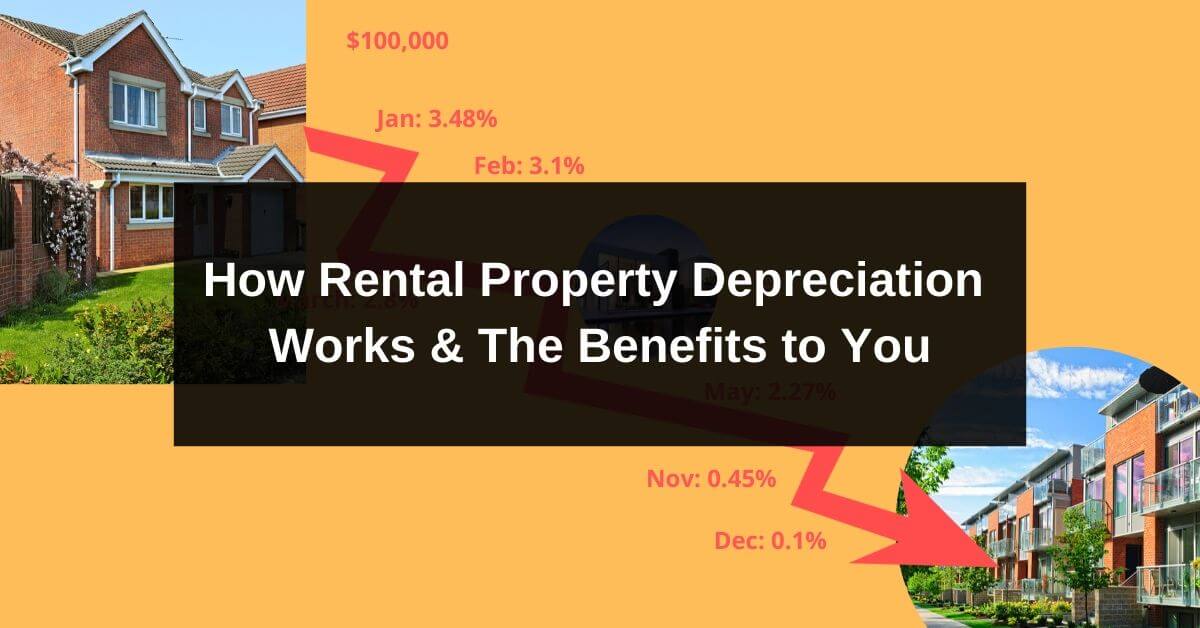

How Rental Property Depreciation Works The Benefits To You

Rental Property Depreciation Rules Schedule Recapture

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

How The New Tax Law Affects Rental Real Estate Owners

Real Estate Investing Frequently Asked Questions Most Common Faqs Real Estate Rentals Renting Out Your House Rental Property

However there is an aspect of the appraisal fee that could be considered an ordinary and necessary expense of doing business in this case.

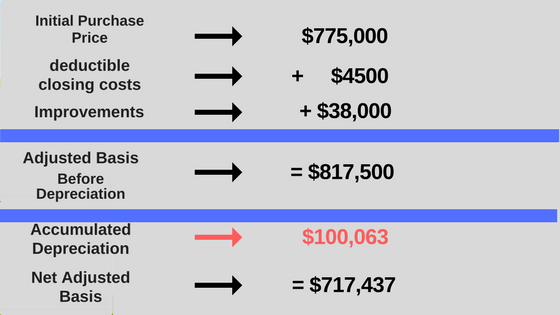

Roof depreciation life rental property. Depreciation starts when you bring the new roof into service. When compared to the alternative option of depreciating the cost over a 27 5 year life for residential rental real estate or a 39 year life for commercial real estate under the modified accelerated cost recovery system an incorrect conclusion may lead to a significant overpayment of tax liability. Correct normally these are either added to the basis or amortized over the life of a loan. The deduction to recover the cost of your rental property depreciation is taken over a prescribed number of years and is discussed in chapter 2 depreciation of rental property.

Generally each year you will report all income and deduct all out of pocket expenses in full. These are the useful lives that the irs deems for both types of properties. Rental property depreciation is calculated over 27 5 years for residential property and 39 years for commercial property. Are generally depreciated over a recovery period of 27 5 years using the straight line method of depreciation and a mid month convention as residential rental property.

Depreciation ends after 27 5 years when you have fully recovered the cost of the new roof. If the property is unoccupied you bring the roof into service when you next lease the rental property. Can i use a special depreciation allowance for a new roof for a rental property.

8 Proven Ways To Feel Safe And Secure With Tenants In Your Own Home Landlording Investment Property For Sale Rental Property Income Property

23 Items For Depreciation On Your Triple Net Lease Property Net Lease Tax Deductions Capital Gains Tax

Why Depreciation Matters For Rental Property Owners At Tax Time Stessa

Calculating Your Profit When Selling Your Rental Property Mortgage Blog

Legalaccomplished Rental Property Tax Deductions Worksheet Rentalproperty

Pdf Download The Landlord S Financial Tool Kit Full Pages By Michael C Thomsett

Depreciation Recapture What Is It And How Can I Reduce It

4562 Half Year Mid Month And Mid Quarter Conventions 1120 1120s 4562

Tax Depreciation Schedules Australia One Of The Least Benefit Of Property Depreciation Is That They Are Non Cash Deductions It Means Tax Deduction Legal Rule

Real Estate Tax Depreciation Basics Millionacres

What Is Rental Property Depreciation

Rental Property Depreciation Reducing Your Tax Burden 37parallel Com

Buyer Contact Form Black Real Estate Forms Realtor Forms Real Estate Agents Realtors Real Estate Marketing Active Real Estate In 2019 Real Estate Forms Real Estate Buyers Real Estate Investing

Turbotax Guide To Tax Deductions For Rental Property Depreciation Thestreet

850 Bunker Hill Boulevard Jacksonville Fl 32208 Hotpads Bunker Hill Renting A House Historic Properties

Us Expat Taxes Explained Rental Property In The Us Us Expat Taxes Explained Rental Property In The Us

Jessy Milner And How He Made 86 000 On His First Deal Livin The Dream Epic Real Estate Investing Podcast In Real Estate Education Real Estate Investing

Florida New Construction Rebate Program New Construction House Hunting Checklist Resources For Home Buyers Room Ideas Home Buying Tips Home Inspection

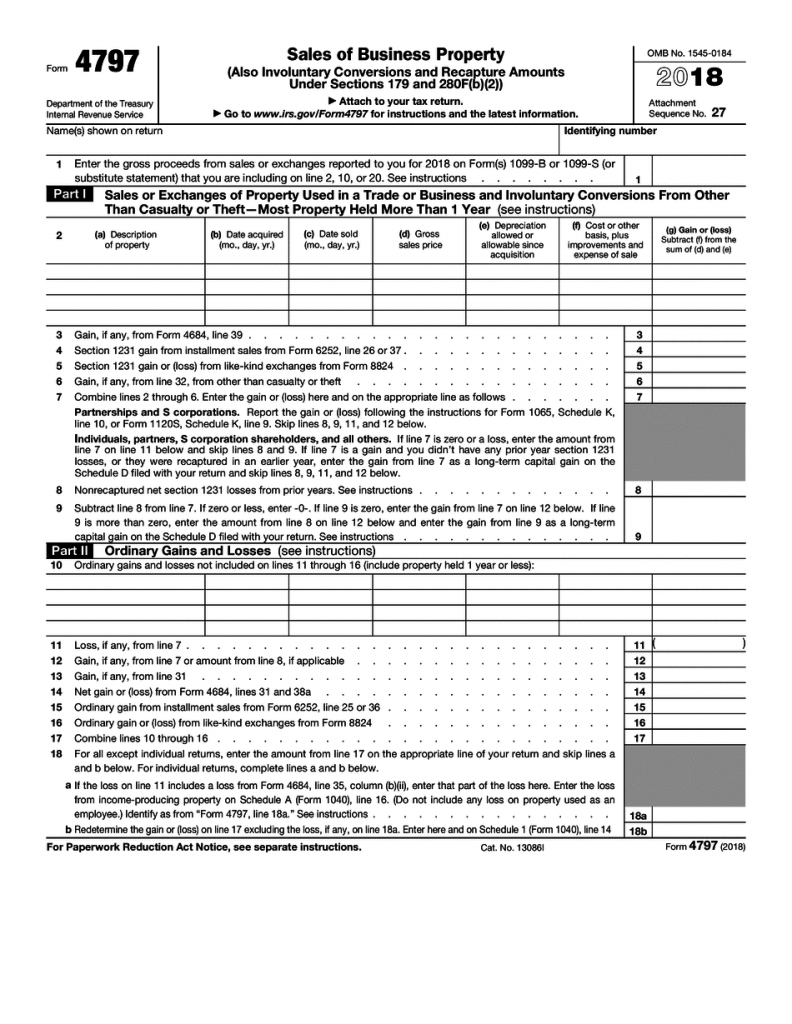

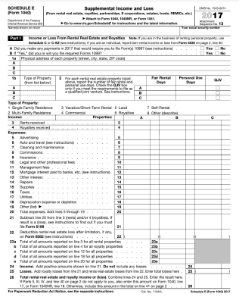

1

Roofing Contract Template 145 Roofing Contract Contract Template Roofing

Pet Care Center Life Petinsuranceplans How To Feng Shui Your Home Buying Your First Home

What If You Forgot To Depreciate Your Rental Property Ipropertymanagement Com

Http Carrstax Com Carrstax Images Rental 20property 20organizer 20worksheet 1 Pdf

Prateek Grand City Bharosa Jyada Prateek Ka Vaada With Images Property Valuation Melbourne City

How To Calculate Taxable Income On Rental Properties 10 Steps

The Dirt On Property Depreciation Property Investment Property Tax Time

1 Bed 1 Bath 800 Sq Ft House For Rent Phoenix North Az 85022 With Images House For Lease Renting A House Arizona House

Keep Your Home Safe While You Re Away Before You Leave For A Trip Take Some Time To Put Dicas De Imoveis Sonho Da Casa Propria Como Comprar Uma Casa

What Is Rental Property Depreciation And How Does It Work

If You Find The Tax Amount For Your Residential Asset Is A Bit Too High Then You Always Have The Right To Ge With Images Investment Firms Property Investor Mortgage Loans

The Irs S Dirty Little Secret About Rental Properties By Becky Harding Medium

Tenancy Fees Explained In 2020 Roof Maintenance Trendy Home Pretty House

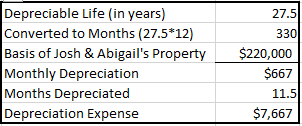

Depreciable Life Life Expectancy For Rental Purchases

Saint Lucie County Property Appraiser S Virtual Office Property Tax

Is This Famous Pulp Fiction Filming Location Prepping For Destruction Filming Locations Pulp Fiction Los Angeles Real Estate

The Secret To Winning A Real Estate Bidding War Renting A House Finding A House Find Houses For Rent

Does Taking A Depreciation Of Rental Property Hurt Me When I Sell Home Guides Sf Gate

How To Deduct A Deck Building A Deck Deck Deck Design

Fancy Living In The Countryside Message Us About This Listing Now Real Estate Website Edmonton

Everyone Wants A Piece Of Land It S The Only Sure Investment It Can Never Depreciate Like A Car Or A Washing Machine L Mortgage Rates Home Mortgage Mortgage

How To Waterproofing Your Home Blog Radhedevelopers Real Estate Companies Real Estate Projects

Paying Back Depreciation On A Rental Property Home Guides Sf Gate